The Future of Fintech Growth: McKinsey Analysis 2023

Fintech growth then and now

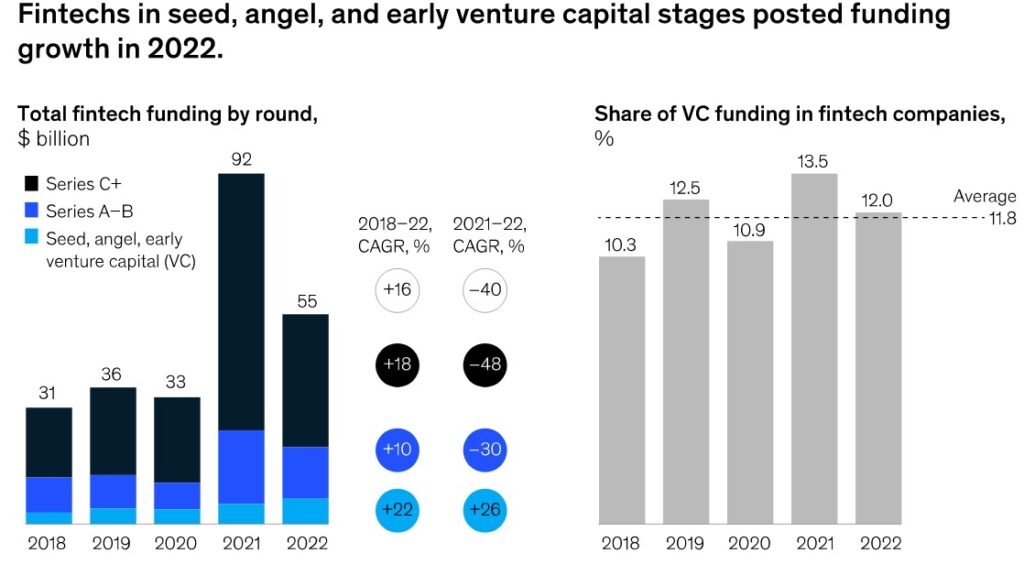

The fintech industry raised record capital in the second half of the last decade. Venture capital (VC) funding grew from $19.4 billion in 2015 to $33.3 billion in 2020, a 17 percent year-over-year increase (see sidebar “What are fintechs?”). Deal activity increased in tandem, with the number of deals growing 1.2 times over this period.

The funding surge proved to be a one-off event. Funding levels in 2022 returned to long-term trend levels as inflated growth expectations from the 2021 extraordinary results were reanchored to business-as-usual levels, and as deteriorating macroeconomic conditions and geopolitical shocks destabilized the business environment. The correction caused fintech valuations to plummet. Many private firms faced down rounds, and publicly traded fintechs lost billions of dollars in market capitalization. VC funding was hit hard globally and across sectors, dropping to $459.6 billion in 2022 from $683.1 billion in 2021. Fintech funding faced a 40 percent year-over-year funding decline, down from $92 billion to $55 billion. Yet, when analyzed over a five-year period, fintech funding as a proportion of total VC funding remained fairly stable at 12 percent, registering only a 0.5 percentage point decline in 2022.

Radical transformation of the banking industry

Banking is facing a future marked by fundamental restructuring. As our colleagues wrote recently, banks and nonbanks are competing to fulfill distinct customer needs in five cross-industry arenas in this new era: everyday banking, investment advisory, complex financing, mass wholesale intermediation, and banking as a service (BaaS).3